top of page

Modern Quant's Gauntlet: Navigating APIs, AI, and C++ for Algorithmic Trading Supremacy

This chasm between a theoretical model and a robust, live trading system is the gauntlet for Algorithmic Trading that every serious trader must run. It is a path littered with technical hurdles, API idiosyncrasies, and the constant, nagging fear of system failure at a critical moment.

Bryan Downing

Nov 21, 202516 min read

Deconstructing a Quantitative Trading Strategy: A Deep Dive into a Browser-Based HFT Backtesting Engine

In the world of finance, High-Frequency Trading (HFT) and quantitative analysis have long been the exclusive domains of sophisticated hedge funds and investment banks with vast resources.

Bryan Downing

Nov 17, 202519 min read

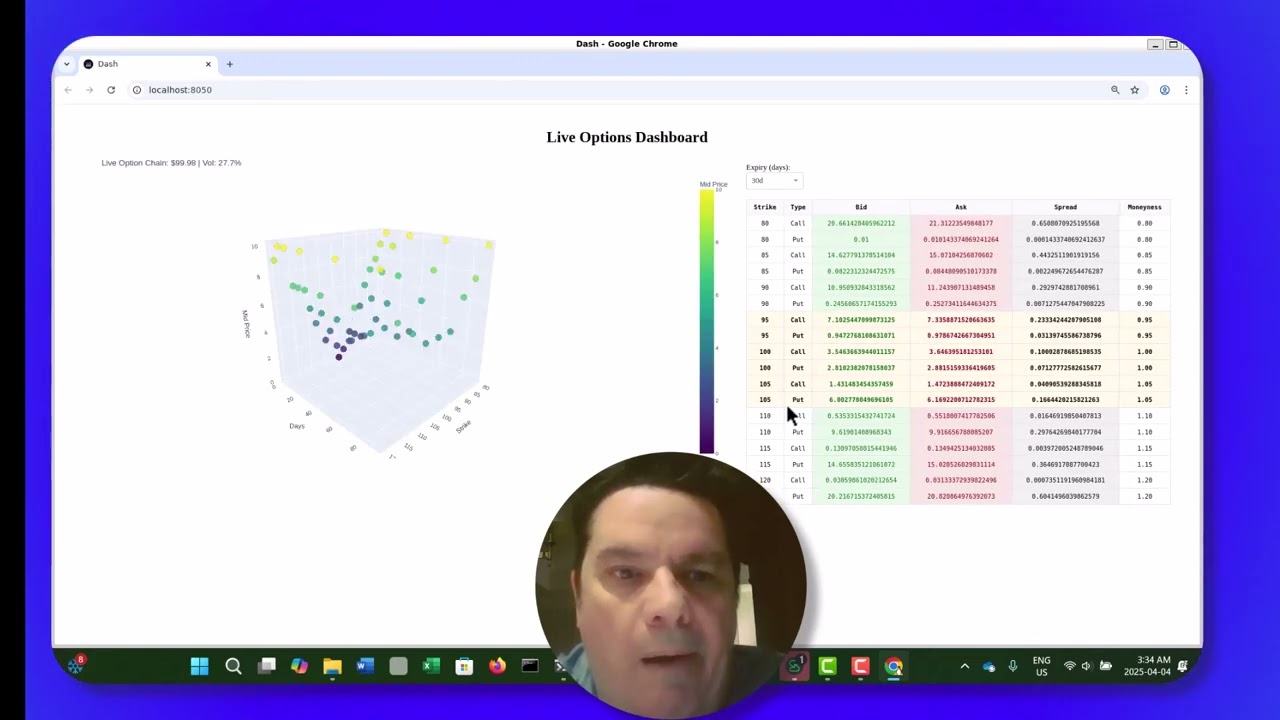

Strategic Alpha with NVDA Option Chain Data for Quant Researchers and HFT

For quant researchers and HFT participants, access to and analysis of real time NVDA option chain data, particularly with modern visualizati

Bryan Downing

Apr 4, 20255 min read

Are High-Frequency Trading HFT Backtesting Frameworks Worth the Investment?

The experimental high frequency trading HFT backtesting framework, as described in the provided features, represents a significant advanceme

Bryan Downing

Oct 23, 20242 min read

bottom of page